Oil trading

All sales were initially made under contract – with an agreed quantity delivered to a specific buyer at a specified time and price. Logistics were important, and margins of error on delivery dates were small.

An important constraint was that the discharging ports had to be reasonably close to the field to ensure that shuttle tankers were always available, thereby avoiding full storage cells and a halt to production. In practice, this meant that these vessels could only serve refineries within the North Sea basin.

It was quickly discovered that contract sales failed to secure optimum prices for Statfjord’s crude oil. The spot market – where each cargo is sold to the highest bigger – was more lucrative, but made greater demands as well.

Contract sales give stable prices because deliveries involve predetermined volumes at a fixed rate over a lengthy period – months or years as is normal in the Middle East, for instance. However, the spot market can often yield higher returns because suppliers can exploit fluctuations in both prices and demand.

The Statfjord crude was a particularly good grade in terms of European product specifications. That made it attractive both as a main product and for blending with cheaper crudes of “poorer” quality – such as heavier oils from the Middle East.

Two factors are important for determining spot prices. The first is the price of Brent Blend, and the other is the quality differential in relation to that reference crude.

Set daily by independent publications in London, the Brent Blend price is the reference point for crudes from the North Sea. Market prices are typically an average of the reference prices on the day the cargo was loaded on the field and two days before and after that point – in other words, a five-day average.

The quality differential is the supplement or deduction which traders can determine on the basis of quality, quantity and buyer requirements. Statfjord crude had a particularly good quality, with a low sulphur content.

Oil from Statfjord remains the property of the partnership until it passes through the loading hose from the buoy and enters the tanker. Ownership then transfers to the relevant licensee.

In practice, however, the cargo is sold once it has been loaded. This means that a buyer on cif terms (which are normal for shipments by shuttle tanker) takes over the ownership and risk at exactly the same moment. The licensees accordingly never own a cargo once it has been loaded into the tanker.

Some of the biggest companies in the Statfjord partnership had substantial refining capacity and extensive distribution organisations, which also meant they had a big demand for crude.

They were accordingly interested in “buying” their own share of the field’s crude. High taxes on oil production in Norway and low taxes on refined products in Europe, where their refineries lay, made it advantageous for them to sell oil at a low price.

Statoil was in the opposite position – large production and little or no refining capacity of its own – and naturally wanted the highest possible price for its crude.

This imbalance was naturally noticed, and eventually also led to changes to conditions and restricted opportunities for each company to deviate significantly from the “average” oil price.

Because Statoil was also instructed later to sell the Norwegian government’s directly-owned share of offshore oil output, the company ranked for a time as the world’s largest crude trader.

To reduce the negative impact of the restrictions on shuttle tanker range, Statoil built an oil terminal at Mongstad north of Bergen with big storage capacity in artificial rock caverns. This created an even more favourable negotiating position for the company’s traders, although the facility remained almost empty during the first few years.

The opportunity to postpone the sale of individual cargoes and store the crude in anticipation of better times or prices represented a very effective threat.

Down the road, the Mongstad terminal became an important part of the infrastructure for selling crude from Norway’s Troll and Heidrun fields in the North and Norwegian Seas respectively.

oljehandel,

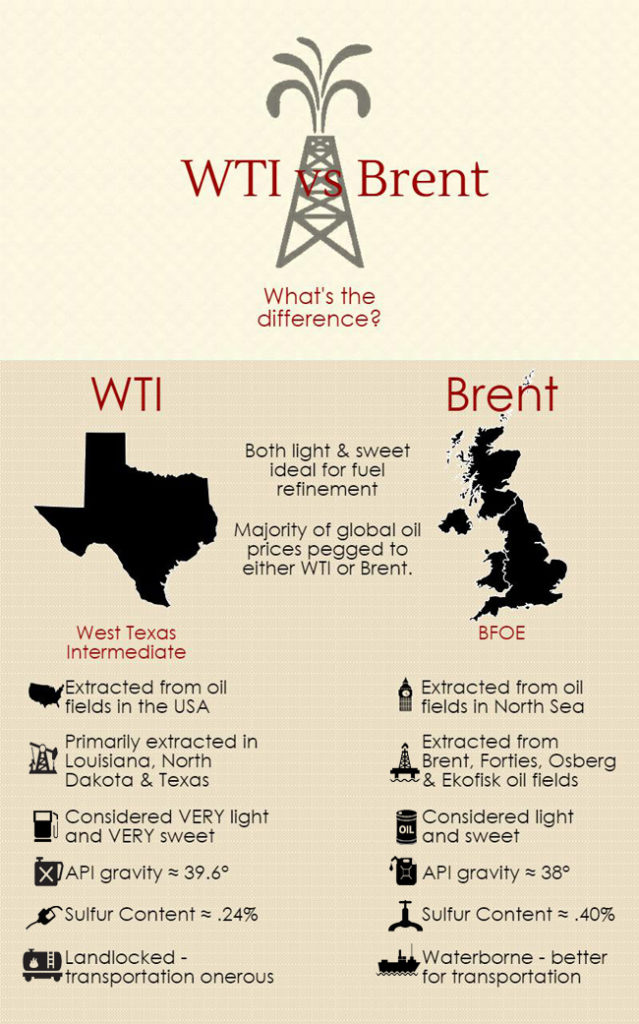

oljehandel,Another reference price used in the USA is West Texas Intermediate (WTI), which is set in the same way as Brent Blend by independent publications on the basis of actual sales prices. As a rule of thumb, the relationship between Brent Blend and WTI was long considered to be freight costs between Europe and the USA. The WTI then had the higher value. But the opportunities available to the Norwegian traders for storing crude at Mongstad and transhipping it to larger tankers meant it was also possible to compete over deliveries to the US.

A few years later still, Statoil’s trading department also began to compete very successfully in the Asian market on the basis of the knowledge gained from selling Statfjord oil.

Supplies from that field and the company’s role as the seller of the government’s oil meant that Statoil ranked for a time as the world’s biggest player in the global spot market for crude.

Sources:

Interview with Gunnar Sletvold.

Ministry of Petroleum and Energy. Oljemarkedet og Norge